Challenges Grew on the Eve of the Iran War; Russia Will Benefit from Higher Energy Prices

KSE Institute has published the March issue of the Russia Chartbook: «Challenges Grew on the Eve of the Iran War; Russia Will Benefit from Higher Energy Prices». The latest issue suggests that the escalation of the conflict in the Middle East has become an unexpected financial lifeline for the Russian economy.

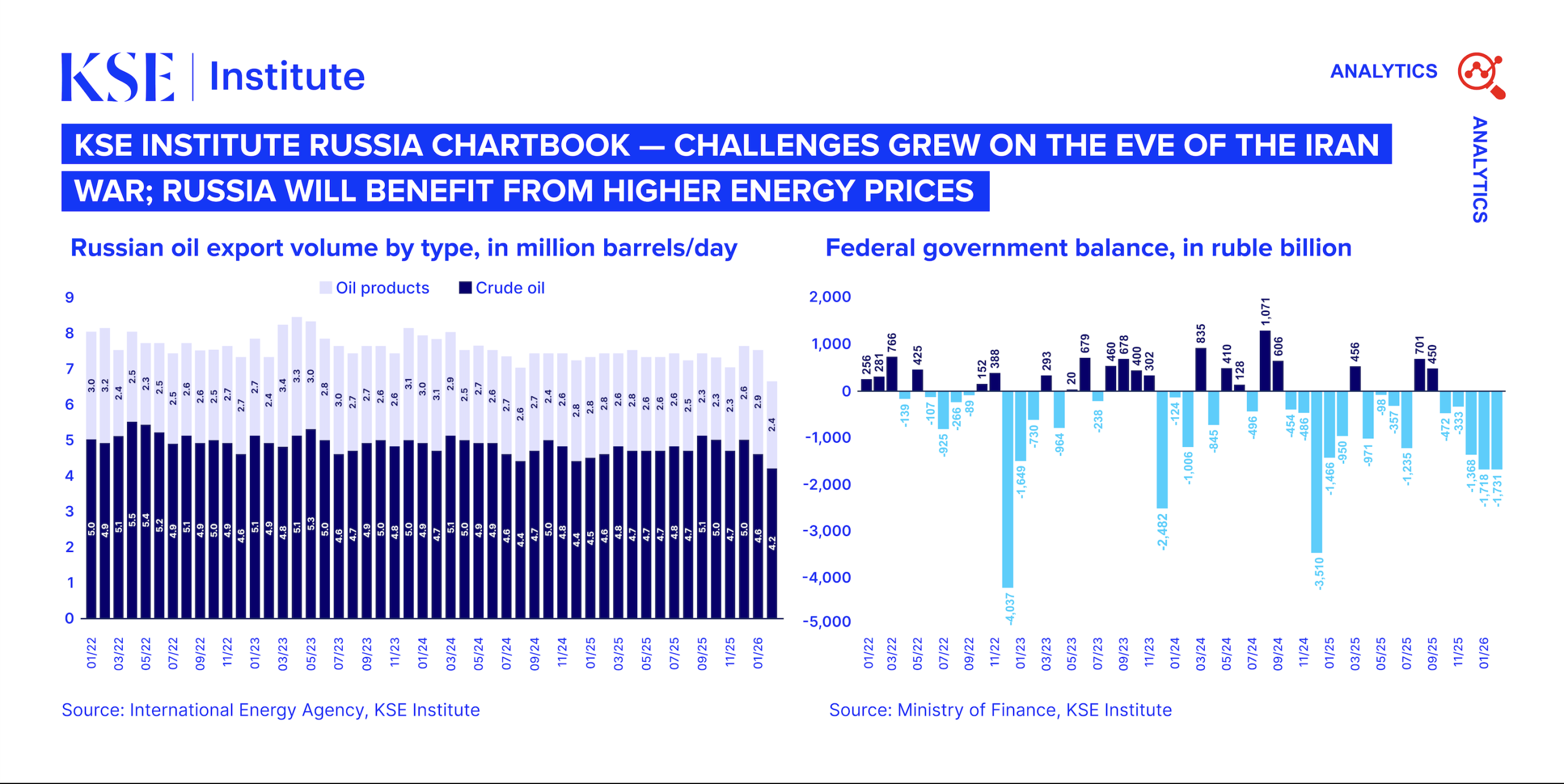

Soaring global energy prices and partial sanctions relief are creating an unexpected windfall for Russia. The escalation in the Middle East has disrupted oil and gas production in the Gulf and significantly constrained flows through the Strait of Hormuz, which accounts for around 20% of global oil and LNG trade, pushing energy prices sharply higher. Russia is already benefiting from both higher prices and the easing of US oil sanctions. If the conflict persists, export earnings and oil and gas budget revenues could increase significantly, easing existing fiscal pressures and undermining efforts to constrain Russia’s ability to finance its war against Ukraine. Continued disruptions, including damage to regional energy infrastructure, increase the likelihood of prolonged volatility in global markets.

At the same time, Russia entered this period in its most vulnerable position in four years. In February, oil export earnings fell to $9.5 billion — the lowest level since the Covid period. For the first time since the full-scale invasion, both export volumes and production declined, by 0.9 mb/d and 0.7 mb/d, respectively, reflecting US pressure on key buyers of Russian oil. This more than offset the effect of somewhat higher export prices driven by rising geopolitical tensions. Budget dynamics also deteriorated: oil and gas revenues in January–February were 47% lower year-on-year, contributing to a record deficit of 3.45 trillion rubles in just two months. Under these conditions, authorities were considering significant spending cuts, while budget financing was becoming increasingly challenging. Persistently low oil prices would also have required adjustments to the fiscal rule, and a review of the 2026 federal budget would likely have been unavoidable.

Structural vulnerabilities remain significant. Domestic federal debt has nearly doubled since the start of the full-scale war, approaching 31 trillion rubles by early 2026. Further OFZ issuance is becoming more difficult, requiring continued support from the Central Bank through repo operations to sustain demand from domestic banks. With the key policy rate reduced to 15.0%, the Ministry of Finance has shifted toward fixed-coupon OFZs as financial institutions lose appetite for floating-rate instruments. At the same time, international reserves are under pressure from declining gold prices, which had previously supported them. Facing tightening liquidity constraints, Russia has begun selling monetary gold, gradually reducing its macroeconomic buffers.

Contacts