Stepping-Up Economic Sanctions Is Urgently Needed To Constrain 🇷🇺

KSE Institute has released its new July Russia Chartbook “Stepping Up Economic Sanctions Is Urgently Needed To Constrain Russia.” Energy sanctions continue to face challenges, while Russia’s favorable external environment supports its economy and fiscal stability. These trends clearly show that the pressure on Russia is insufficient. Ukraine’s allies must demonstrate their political will and ensure that sanctions work to their full potential.

In June 2024, almost 90% of Russian seaborne crude oil exports were transported by shadow fleet tankers, further weakening the G7/EU price cap regime. As a result, Russian oil export earnings in the first half of 2024 increased by 22% compared to the same period in 2023, when sanctions were more effective. While sanctions on individual shadow tankers have removed many from operations, they have not significantly impacted Russian oil prices. Of the 55 shadow fleet tankers sanctioned by the US, EU, and UK, 41 remain idle. We believe that scaling up the number of targeted tankers and punishment of potential violators are essential to increase the effectiveness of these sanctions.

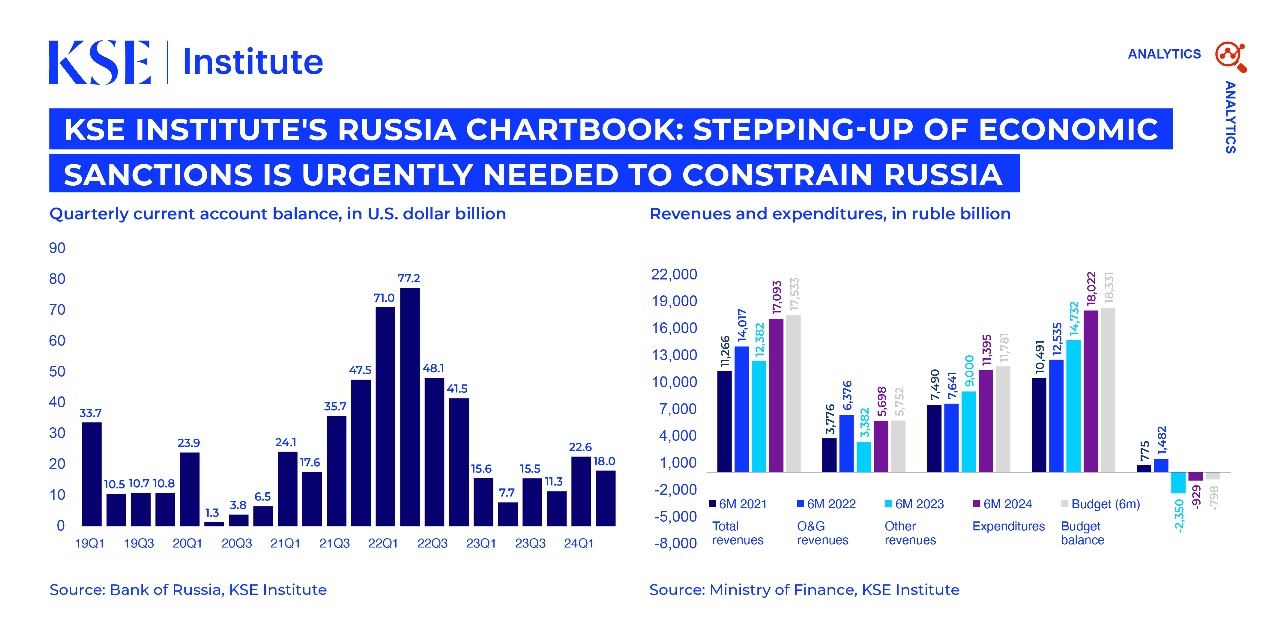

High profits have contributed to a favorable environment, ensuring Russia’s macroeconomic stability. In the first half of 2024, Russia’s trade balance reached $68 billion, a 19% increase compared to the same period in 2023. The overall current account surplus rose to $41 billion, a 74% increase. Although non-oil exports were weaker, lower imports and a smaller income and transfers deficit supported the current account. These favorable conditions reduced pressure on the ruble, leading to its strengthening. This was further supported by interest rate hikes from the Central Bank of Russia since mid-2023. Less effective energy sanctions have allowed Russia to maintain economic stability.

Russia is not facing major fiscal constraints. In the first half of 2024, Russia’s federal budget deficit reached 929 billion rubles, 58% of the full-year target and 60% less than the same period in 2023. Higher revenues from oil and gas (+69%) and non-oil and gas (+27%) more than covered the increased spending (+22%) due to higher war costs. Russia is on track to meet its 2024 target, and at current oil export prices, it is unlikely to face significant external imbalances or budgetary issues. Nonetheless, the government is considering significant tax increases to create more policy space, and is facing challenges with internal borrowing due to unfavorably high rates.

Vulnerabilities remain due to reduced macroeconomic buffers. If sanctions on Russian energy exports are tightened, including measures to curb the shadow fleet, Russia’s weaknesses could quickly resurface. Since the start of the full-scale invasion, Russia has spent nearly $54 billion of the National Wealth Fund’s liquid assets, leaving only gold and yuan, which cannot easily be used to finance the budget. This would force the government to rely on higher domestic debt issuance, driving up borrowing costs even further. In addition, the immobilization of around $300 billion in Central Bank reserves limits Russia’s options.

Contacts