Weaker Global Oil Prices Create An Opportunity To Exploit Vulnerabilities; Budget Reflects Commitment To War

KSE Institute has released its new October Russia Chartbook “Weaker Global Oil Prices Create An Opportunity To Exploit Vulnerabilities; Budget Reflects Commitment To War.” Ukraine’s allies should take advantage of Russia’s macro imbalances and step up sanctions pressure. A further reduction in export earnings would weaken the currency and increase inflationary pressures.

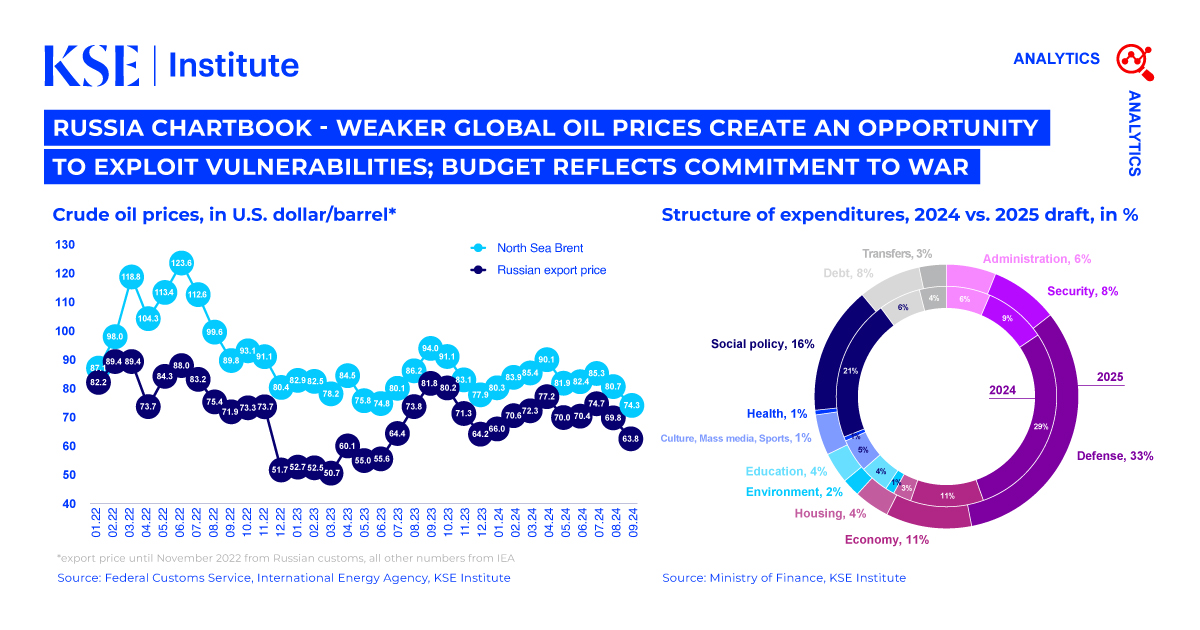

In September, Russia’s oil exports fell to $14.7 billion, the lowest since mid-2023, due to a sharp drop in global oil prices, not sanctions. The average price of Russian oil fell from nearly $75 per barrel in July to $70 in August and $64 in September. The discount to Brent remained stable at $10-11 per barrel, the lowest level since the start of the full-scale invasion.

Despite lower oil revenues, Russia’s current account surplus reached $50.6 billion over the first nine months of 2024, up 30% from the same period in 2023. This increase was driven by stable goods exports, with oil revenues offsetting lower non-oil exports, and a $15 billion year-over-year drop in imports. Russia’s use of shadow fleet tankers to evade the EU/G7 oil price cap allowed it to earn an extra $10 per barrel, adding about $8 billion in extra earnings.

Russia’s federal budget reached a 169 billion ruble surplus from January to September, a major shift from the 1.5 trillion ruble deficit last year. Higher oil and gas revenues (+49%) and other revenues (+27%) balanced a 23% spending increase, keeping Russia on track for its 2.1 trillion ruble deficit target for 2024. Despite declining NWF reserves and rising interest rates, limited fiscal financing needs continue to support budget stability. The 2025 budget shows a strong commitment to military spending, projected to reach $140 billion, up from $118 billion planned for 2024.

However, inflation remains a key challenge for Russia, leading the CBR to raise its key interest rate to 21% in October. This marks a cumulative increase of 13.5 percentage points since mid-2023, bringing the rate above the levels in February-March 2022. This increase responds to strong inflationary pressures: a tight labor market driving real wage growth near double digits, high war-related spending, expanding private sector credit, and a weaker ruble. While higher rates should help curb inflation, they also risk slowing the economy, adding to Russia’s fiscal challenges amid reduced reserves and limited policy options.

Contacts