Macroeconomic Pressure On Russia Remains Moderate

KSE Institute has published its June Russia Chartbook “Macroeconomic Pressure On Russia Remains Moderate.” High oil prices and weak price cap enforcement support Russian exports, while improved external dynamics help maintain macroeconomic stability. It is crucial for Ukraine’s allies to improve the enforcement of sanctions against Russia to effectively undermine its war efforts in Ukraine.

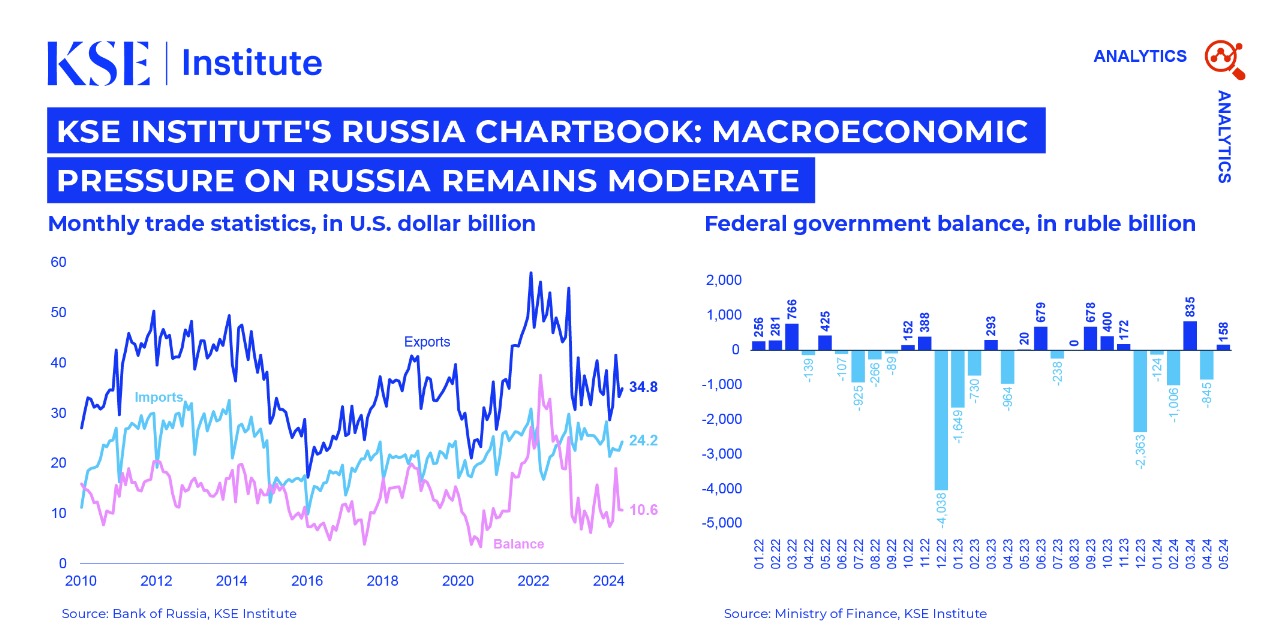

KSE Institute has published its June Russia Chartbook “Macroeconomic Pressure On Russia Remains Moderate.” High oil prices and weak price cap enforcement support Russian exports, while improved external dynamics help maintain macroeconomic stability. It is crucial for Ukraine’s allies to improve the enforcement of sanctions against Russia to effectively undermine its war efforts in Ukraine.

While global oil prices declined somewhat in May, with Brent crude falling to $82 per barrel, these prices remain higher than at the end of 2023. This increase more than compensates for the wider Urals discount resulting from OFAC’s vessel designation strategy. Furthermore, there are additional challenges emerging. First, Russia has successfully replaced nearly 90% of the tanker capacity that was removed. Second, some of the vessels in question appear to be returning to commercial service. To maintain credibility, OFAC will need to initiate enforcement actions against entities interacting with these vessels or their cargo.

These factors are further supported by improved external dynamics, which are contributing to macroeconomic stability and strengthening the ruble. Russia’s trade surplus remained stable in May, aiding the overall current account to reach $38.1 billion for the first five months of the year. This marks an over 80% increase compared to the same period in 2023, potentially leading to a full-year surplus of approximately $90 billion if current trends continue. The more favorable external environment, combined with the Central Bank of Russia’s (CBR) monetary policy response—a cumulative 850 basis points in interest rate hikes—has resulted in a moderate recovery of the ruble exchange rate.

These strong revenues have allowed Russia to avoid significant fiscal constraints despite increased spending. In the first five months of the year, the federal budget deficit reached 1.0 trillion rubles—62% of the full-year target but less than one-third of the same period in 2023. Substantially higher revenues (+46%)—including oil and gas (+74%) and non-oil and gas (+34%)—have more than compensated for the increased spending (+19%) due to higher war expenditures. At current oil export prices, Russia is unlikely to face significant external imbalances or budgetary constraints. However, the government is considering significant tax increases to reduce its reliance on oil and gas revenues.

Nevertheless, vulnerabilities exist due to reduced macroeconomic buffers as sanctions limit access to reserves. If increased economic sanctions successfully reduce energy revenues in the coming months, Russia’s underlying vulnerabilities could quickly resurface. Since the start of the full-scale invasion, Russia has spent nearly $54 billion of the National Wealth Fund’s (NWF) liquid assets, leaving only gold and yuan, which cannot be easily used at scale to finance the budget. This would force the regime to rely on higher domestic debt issuance, increasing borrowing costs. Additionally, the immobilization of nearly $300 billion in Central Bank of Russia (CBR) reserves severely limits policy options.

Contacts